U.S. Housing Markets Still Searching for Peak Prices

File Photo: Boise, Idaho - Getty images

FAU Economist: Homeownership No Sure Thing for Wealth Creation

By Paul Owers, FAU Media Relations

BOCA RATON, Fla. (Feb. 23, 2022) - Higher mortgage rates have yet to cool overheated housing markets across the country as prices continue a steady climb in each of the nation's 100 largest metropolitan areas, according to researchers at Florida Atlantic University and Florida International University.Each month, FAU's Ken H. Johnson, Ph.D., and FIU's Eli Beracha, Ph.D., rank the most overvalued housing markets of America's 100 largest metros.

Johnson and Beracha incorporate average or expected price changes and provide an estimate of how much a market's housing stock is over- or undervalued, relative to its historic pricing.

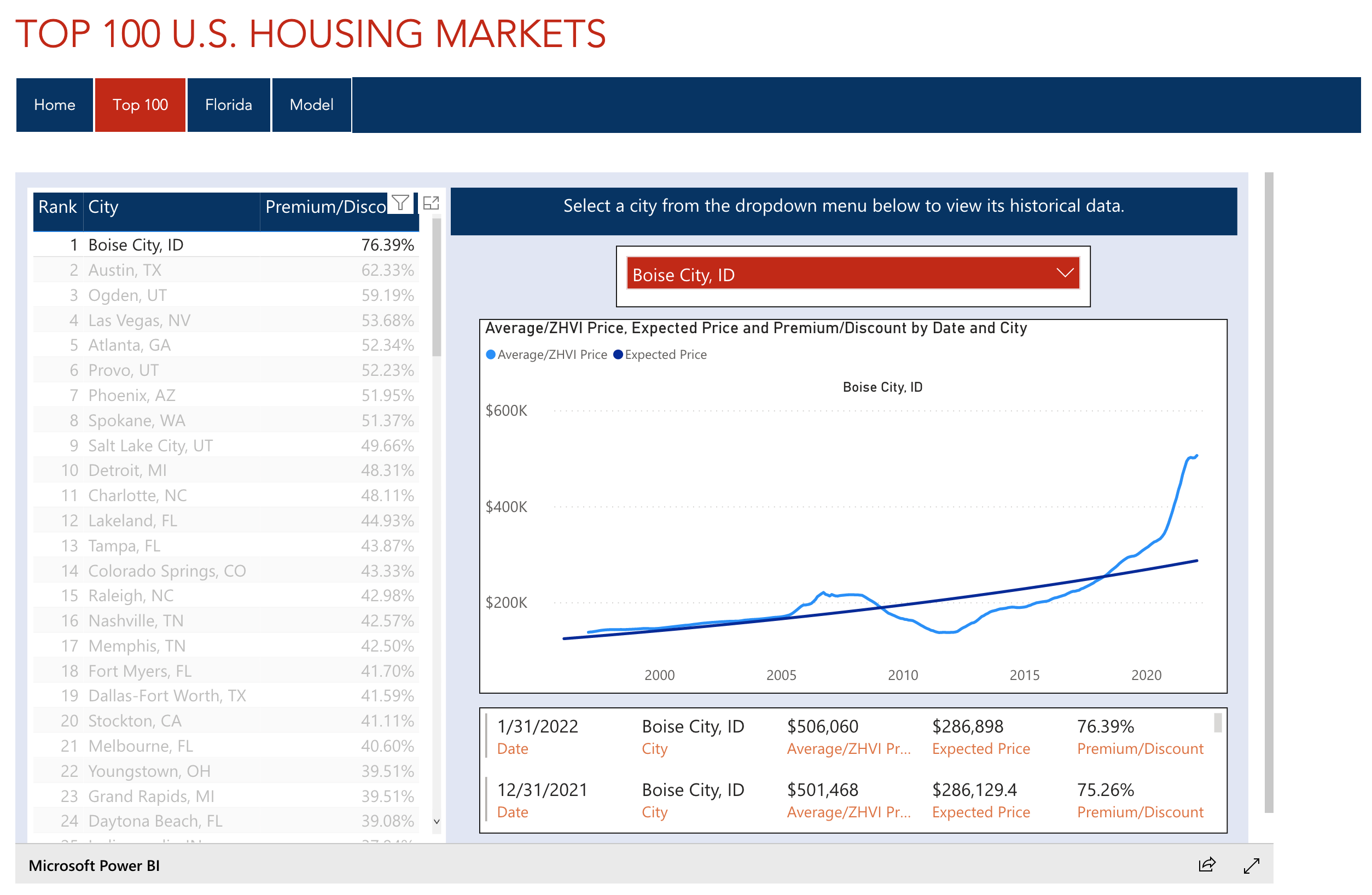

As of January, price premiums are up from December 2021 in all 100 markets, including Boise, Idaho, the nation's most overvalued market. Boise buyers paid a premium of 76.39 percent last month, while buyers in No. 2 Austin, Texas, paid a premium of 62.33 percent. Meanwhile, Las Vegas and Atlanta are rising in the top 10, with both markets more than 50 percent overvalued.

Two months ago, "pricing crowns" were developing in Los Angeles, San Francisco and other Western U.S. metros, an indication that the long-anticipated housing slowdown was starting. Today, however, prices have reaccelerated in all but a few of those Western metros.

In none of the 100 markets are homes considered undervalued, based on historical pricing. The data, which extends from January 1996 through the end of January 2022, includes single-family homes, townhomes, condominiums and co-ops.

The full rankings with interactive graphs can be viewed by clicking here [FAU College of Business]:

Ideally, housing values fluctuate moderately around a long-term, upward-sloping pricing trend, according to Johnson. Moderate fluctuations around this trend have made homeownership a wealth-generating engine for millions of middle-class Americans.

"With modest fluctuations, people could buy, regardless of the point in a housing cycle and know that within a few years their ownership would create noticeable wealth," said Johnson, an economist with FAU Executive Education in the College of Business. "But with the dramatic fluctuations that we're seeing now, wealth creation through housing is not guaranteed, making homeownership a sometimes-risky investment."

To illustrate the point, Johnson compared current home prices in metropolitan Miami to those at the peak of the housing bubble in the mid-2000s.

In November 2006, Miami homebuyers paid on average $339,762, but it would not have been until May 2021 that they could have sold for a higher price ($343,879). And even then, after 15 years, the price gain would have been less than $5,000.

"Using our data, buyers can make similar comparisons in the other 99 housing markets," Johnson said. "It's clear that purchasing at the peak of a housing cycle is devastating to wealth creation."

Johnson and Beracha say the next few months are crucial for housing markets across the country.

"We encourage buyers to negotiate aggressively or to consider renting, even in light of the recent surge in rental rates," said Beracha, of FIU's Hollo School of Real Estate. "If you lock in a home price now, it could take years to see the return on that investment. Temporarily high monthly rent could be viewed as the cost of avoiding the vagrancies of an irrationally exuberant housing market."

What to Read Next